Developed economies have settled into a new normal of low growth as a result of the structural change from the recent financial crisis. Clayton Christensen and Derek van Bever recently suggested that The Capitalist’s Dilemma explains why growth hasn’t picked back up like after previous recessions and is the leading reason why “despite historically low interest rates, corporations are sitting on massive amounts of cash and failing to invest in innovations that might foster growth“. The thinking behind The Capitalist’s Dilemma also help to understand the delivery-innovation paradox, Missing M in SME, innovation investment decision risk aversion, low R&D spending, innovation investment behaviour by large firms, and Canada’s poor innovation performance. Business leaders need to understand the implications of The Capitalist’s Dilemma because it may lead to the biggest change of all in current times – the end of capitalism – if the current financial orthodoxy does not change.

The Capitalist’s Dilemma

Christensen and van Bever describe the capitalist’s dilemma as “doing the right thing for long-term prosperity is the wrong thing for most investors, according to the tools used to guide investments“. Readers should refer to their article for their complete argument but essentially they blame the confluence of supposedly success oriented finance metrics (RONA, ROIC, RORC, IRR, etc), false sense of correctness from spread sheet models, low loyalty investors, and analysts pressures to force short term business decisions that result in low returns and low growth and a bias against new value creation. Their argument is based on revisiting the basic economic assumption that capital is scarce and costly which drives the backwards looking finance metrics towards the wrong decisions for developed economies at the macroeconomic level but also for long term value creation for investors through firm level innovation.

Explains A Lot

The finance orthodoxies from before the structural change and the capitalist’s dilemma explain much of why business investment in R&D and innovation is so low, the preference for low risk investment decision alternatives, and why Canadian business leaders don’t adopt innovation as a strategy. Economic growth requires innovation but business leaders given the choice are not investing heavily in innovation or if they do are not receiving good results (in terms of top line growth) or think they are innovating a better future by investing in continuous improvement alone. How can we make sense of better outcomes from innovation investments?

Innovation Outcomes and Impact On Growth

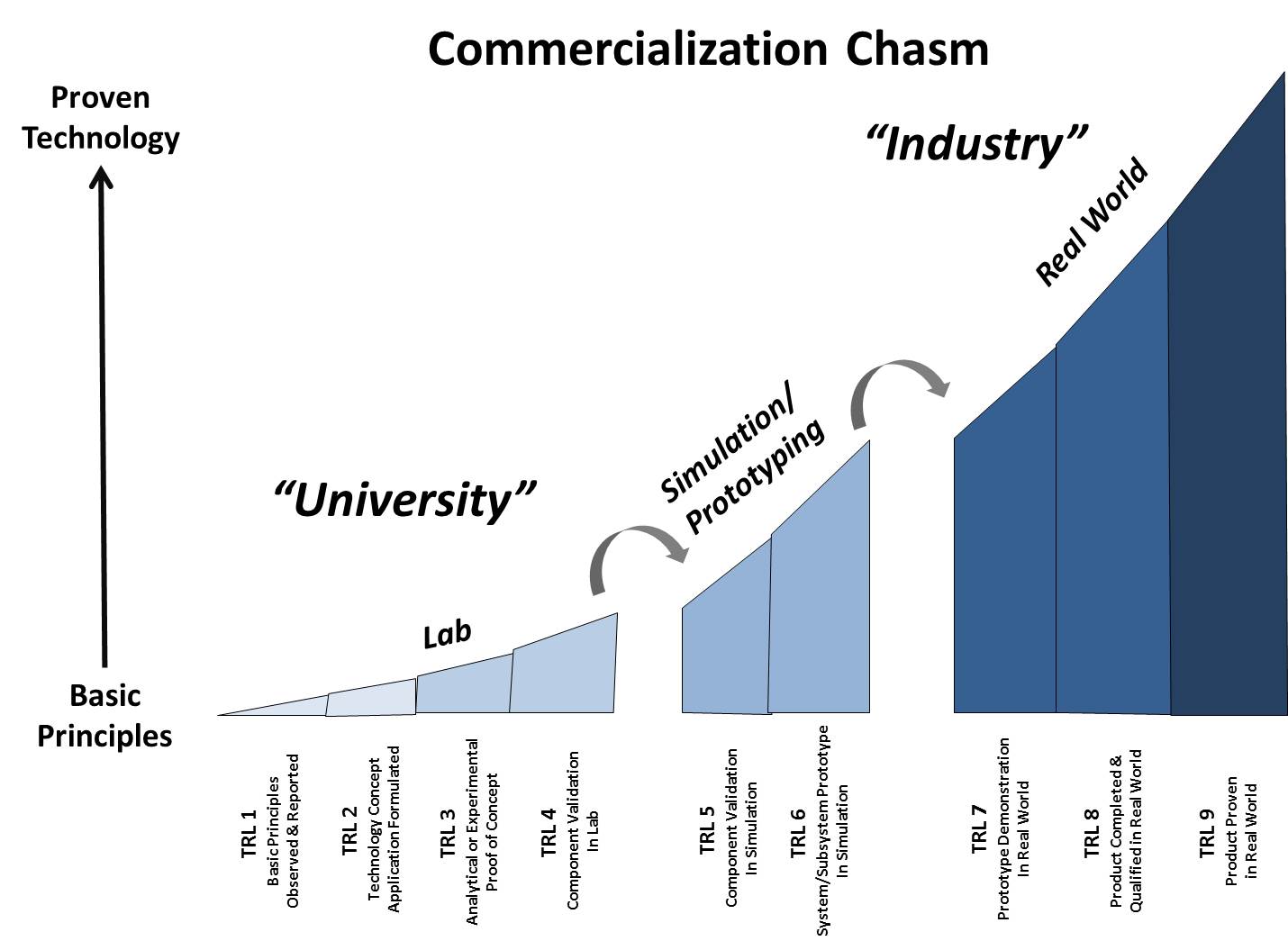

Christensen and van Bever frame innovation in a way that helps to differentiate how different innovation activities(R&D, business model innovation, new product development) , emphasis, and investments lead to positive growth outcomes or not. By categorizing innovation by outcome (be it top-line revenue growth or more jobs) they propose three categories and how each impact growth:

- Performance Improving Innovation – Innovation that replaces old products with new and better models. The impact of performance improving innovation are substitutive in the market place that don’t drive growth.

- Efficiency Innovation – Innovation that helps companies make and sell mature, established products or services to the same customers at lower prices. The impact of efficiency innovations raise productivity that frees-up capital for more productive uses.

- Market-Creating Innovation – Innovation that transforms complicated or costly products so radically that they create new classes of consumers or a new market. The impact of market creating innovation is growth from new customers. The authors also note that efficiency innovations that turn non-consumption into consumption are market creating innovation.

Using these categories Christensen and van Bever demonstrate that the way that investment assessments are made under the current finance orthodoxy lead to too much performance improving and efficiency improving innovation and with a bias against market-creating innovation. So business leaders say they are investing in innovation by investing in performance and efficiency innovations but these don’t drive growth. To drive growth business leaders need to invest in more market-creating innovation but the finance orthodoxies inhibit this choice. What will it take to change the finance orthodoxies going forward to allow market-creating innovation to flourish?

Actions Going Forward

Developed countries and Canada in particular have several options:

- Do Nothing – Allow existing businesses to not grow and slowly fail and the current generation of business leaders, CEOs, CFOs, financial analysts to go extinct to be replaced by a new generation of leaders and financial in those firms that manage to survive.

- Change The Rules of the Game – Christensen and van Bever identify several:

- Repurpose capital away from migratory and timid capital to enterprise capital through tax policy, loyalty shareholder investment rules

- Rebalancing business schools away from the success financial metrics.

- Appropriate risk adjusted cost of capital for the new structural norm enabling longer term investments.

- Reallocate innovation pipeline emphasis for more market creating innovation rather than heavy weight emphasis on performance and efficiency innovation.

- Emancipating management and reducing the influence of tourist (short term) investors.

The drivers of corporate change over the last several decades now themselves must change. The question is will they follow their own advice or have they become the dinosaurs. Investment in performance innovation and much of efficiency innovation is not good enough going forward.